Decoding Real Rate of Returns

The real rate of return refers to the annual rate of return on an investment after considering the impact of tax and inflation, giving the actual purchasing power of the investment. The raw rate of return that is given by investment vehicles, without taking into consideration the impact of taxation and inflation, is called the nominal rate of return. The returns generally denoted by investment products are nominal rates of return. In essence, the real rate of return is the actual return that you will receive after making an investment.

Post-tax return

The post-tax return of an investment refers to the return that you generate after taking into account the impact of tax. You can calculate the post-tax return with the following formula -

Post-tax return = Nominal rate of return * (1-Tax rate)

The real rate of return gives you a clear picture of the actual returns generated by an investment and can be a useful tool to compare different investment instruments. However, before going any further, it is important to understand what inflation is and why we need to net off inflation when determining returns.

What is the Inflation?

Inflation refers to the decrease in the value of money over a period of time. This results in a rise in prices and a decrease in purchasing power. The average growth in the value of a basket of selected goods and services can be used to calculate the rate of inflation. The real rate of return is generally lower than the nominal rate of return except for the rare scenario of deflation.

Deflation is the exact opposite of inflation and refers to a sustained decrease in the general price level of goods and services, often leading to reduced consumer spending, increased debt burdens, and economic downturns. It can create a cycle of falling demand, rising unemployment, and challenges for central banks in implementing effective monetary policies.

As aforementioned, to determine the accuracy of the returns you will receive in hand and the purchasing power of those returns, you need to net off the impact of inflation.

Formula to Calculate the Real Rate of Return

To calculate the real rate of return, you first need to calculate the post-tax return (PTR)

PTR = Nominal return*(1-Tax rate)

Let’s assume that the nominal return is 12%, and the investor falls into the tax slab of 20%.

Thus, PTR = 12%*(1-20%)

=0.12*(1-0.20)

=0.12*(0.80)

=0.096

=9.6%

Now, to calculate the real rate of return, you need to account for inflation. Let’s assume that the inflation rate is 6%

Real rate of return = ((1+PTR) / (1+Inflation)) - 1

=((1+9.6%)/(1+6%))-1

=(1.096/1.06)-1

=1.034-1

=0.034

=3.4%

Hence, the real rate of return is 3.4%.

Importance of Real Rate of Return

The real rate of return not only gives you an understanding of the actual return you are generating but also helps you choose the right product efficiently. With the real rate of returns, you can determine the exact returns that you can pocket. Moreover, through this, you can compare the real rate of return of different investment avenues and choose the one most suitable for you. Products or asset classes that give you consistently high real returns over a period of time will help you build wealth in the long run.

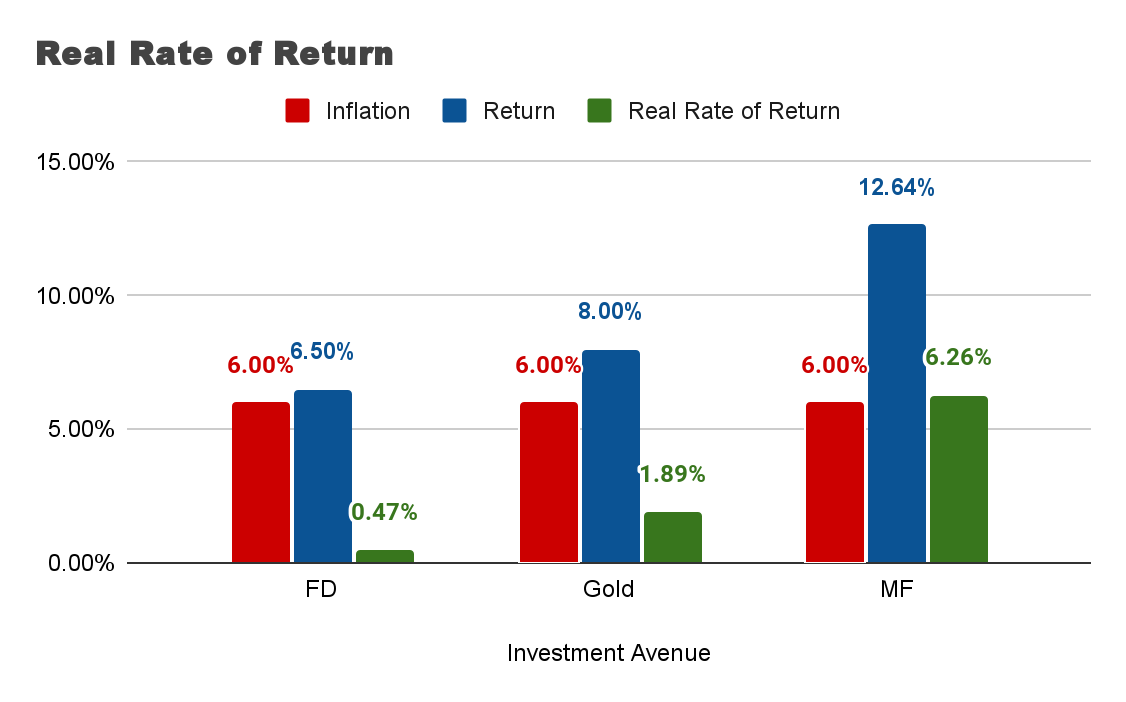

Comparing Different Investment Avenues

Fixed Deposits (FDs)

For a long time, Indian investors have had the tendency to confide in the safety of FDs to protect and generate return on their hard-earned money. However, it is time to ask an important question - is the return really attractive? Let’s assume FDs generate a return of 6.5% and inflation in the same period is 6%. When you adjust this for inflation, the return will shrink to just 0.47%. Furthermore, if you consider the tax impact, the return will be much lower. (The returns on FDs are taxed based on the investor’s tax slab.)

Gold

Traditionally, gold has been a beloved investment avenue in investor portfolios. Let’s assume gold generates a return of 8%. Factoring in the real rate of return, i.e., the post-inflation rate, the return plummets to 1.89%. Furthermore, if you consider the tax impact, the return will be much lower (Assuming inflation to be 6%. For gold, the tax will be dependent on the type of instrument and holding period.)

Equity Mutual Funds

The mutual fund industry is growing at a scorching pace, with its AUM crossing Rs 50 lakh crore in December 2023 (Source - AMFI). With that, mutual funds offer a great investment opportunity, allowing you to not only fulfil financial needs but also build wealth. Let’s assume mutual funds generate returns of 12.64%. Factoring in the impact of inflation, the return would dwindle to 6.26%. However, if you consider the tax impact, the returns will fall further. (For investments held for more than 1 year, long-term capital gains are charged at 10%. This is only applicable on returns of over Rs 1,00,000 per year.)

When we compare the returns generated by equity mutual funds with other investment avenues (FD and Gold), this return is the highest. (Assuming investment in Equity Fund and an average return of 12.64% p.a. as per AMFI Best Practices. Guidelines Circular No. 135/BP/109/2023-24 dated November 01, 2023. Assuming inflation to be 6%).

To conclude, decoding the real rate of returns is essential for investors to make informed decisions about their investment choices. The real rate of return acts as a reliable metric to measure the actual gains, accounting for the impact of inflation on purchasing power. With the availability of a plethora of investment avenues, the real rate of return becomes an indispensable tool for making informed investment decisions.

Disclaimer:The information contained herein is only for information and does not constitute, and should not be construed as investment advice or a recommendation to buy, sell, or otherwise transact in any security or investment product or an invitation, offer or solicitation to engage in any investment activity. Mutual fund investments are subject to market risks, read all scheme-related documents carefully before investing.